Valuing stocks seems like a tough task in itself and more difficult is drawing a line between paying up and overpaying. Here are some insights on this topic I draw from investing legends and their experience.

Charlie Munger said this in his landmark speech titled – A Lesson on Elementary, Worldly Wisdom As It Relates To Investment Management & Business…

Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return—even if you originally buy it at a huge discount.

Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with a fine result.

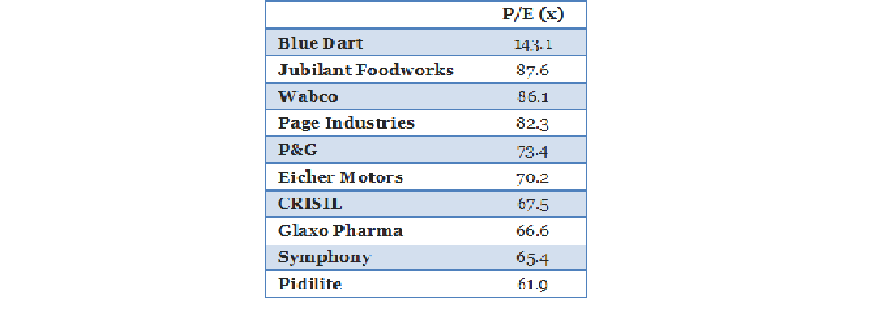

Now, if I were to look at some of the high quality businesses in India, it surely seems that investors are taking Mr. Munger’s idea about paying an “expensive looking price” very seriously. Here are, for instance, the P/E ratios of some high quality businesses…

In Lewis Carroll’s “Through the Looking Glass”, Alice’s finds that she has to run faster and faster just to stay in place.

Well, in our country,” said Alice, still panting a little, “you’d generally get to somewhere else if you run very fast for a long time, as we’ve been doing.

Here’s the advice Red Queen, an antagonist in the story, offers Alice…

A slow sort of country!” said the Queen. “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!

In sum, the Red Queen advises Alice to exert ever more effort just to maintain her current position.

Evolutionary biologist Leigh Van Valen took inspiration from the Red Queen’s words and proposed a principle called the Red Queen Effect in 1973 to explain how, for an evolutionary system, continuing development is needed just in order to maintain its fitness relative to the systems it is co-evolving with.

In biology, this means that animals and plants don’t just disappear because of bad luck in a static and unchanging environment, like a gambler losing it all to a run of bad luck at the casino.

Instead, they face constant change – a deteriorating environment and more successful competitors and predators – that requires them to continually adapt and evolve new species just to survive.

This theory has been applied to explain the relatively high speeds of rabbits and foxes, each of which developed faster running abilities in an attempt to gain respective advantage in the predator-prey relationship between these two animals.

- Spotlight: Big ideas from Value Investing and why applying them in your investment decision making will be a great deal

- InvestorInsights: Interviews with experienced value investors, learners, and deep thinkers

- StockTalk: Thorough analysis of business models of companies (without any recommendations)

- Behaviouronomics: Deep analysis of human behaviour and how it impacts investment decision making

- BookWorm: Reviews of the best books on Value Investing and related subjects

- Free Course – Financial Statement Analysis for Smart People (otherwise priced at Rs 5,900)

- Archives: Instant access to our huge archive from the past three years