Note: This interview was originally published in the December 2016 issue of Value Investing Almanack. To read more such interviews and other deep thoughts on value investing, business analysis and behavioral finance, click here to subscribe to VIA.

“I wish I could talk to this guy,” I told my wife when I read Ben Graham’s The Intelligent Investor first time sometime in 2005.

“But he is dead, right?” she said.

“Oh, not Graham,” I exclaimed, “But Jason Zweig who has edited this version of Graham’s book.”

“I am sure you would one day,” she said with an air of confidence. But I junked her thoughts saying, “Why would he even want to talk to me?”

Well, I had this discussion in mind when I wrote to Mr. Zweig in mid-October last year to request him for an interview for our Value Investing Almanack newsletter. I knew it was a shot in the dark, something I had not done for a long-long time after missing a few such shots in the dark on stocks I lost money owning.

But this shot worked, and worked well for me. Not only did Mr. Zweig agree immediately for the interview, he also made me comfortable by asking me to address him as, well, Jason. 🙂

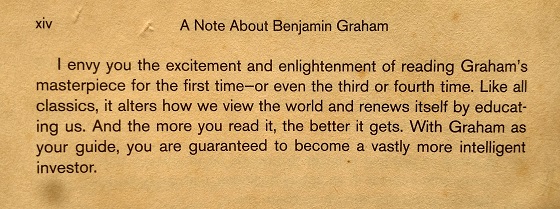

It turned out to be a great interview for me as a learner, and I hope Jason also found it worth his time and effort. Before I begin, I remember this quote from Jason in his starting note for The Intelligent Investor –

In the same way, I envy you the excitement of reading Jason’s thoughts in this interview for the first time. So let’s start right here with a brief introduction.

Jason Zweig is the investing and personal-finance columnist for The Wall Street Journal. He is the author of The Devil’s Financial Dictionary, a satirical glossary of Wall Street (PublicAffairs Books, 2015), and Your Money and Your Brain, on the neuroscience of investing (Simon & Schuster, 2007).

Jason Zweig is the investing and personal-finance columnist for The Wall Street Journal. He is the author of The Devil’s Financial Dictionary, a satirical glossary of Wall Street (PublicAffairs Books, 2015), and Your Money and Your Brain, on the neuroscience of investing (Simon & Schuster, 2007).

Jason edited the revised edition of Benjamin Graham’s The Intelligent Investor (HarperCollins, 2003), the classic text that Warren Buffett has described as “by far the best book about investing ever written.” He also wrote The Little Book of Safe Money (Wiley, 2009); co-edited Benjamin Graham: Building a Profession, an anthology of Graham’s essays (McGraw Hill, 2010); and assisted the Nobel Prize-winning psychologist Daniel Kahneman in writing his book Thinking, Fast and Slow. From 1995 through 2008 Zweig was a senior writer for Money magazine; before joining Money, he was the mutual funds editor at Forbes.

Jason has also been a guest columnist for Time magazine and cnn.com. He has served as a trustee of the Museum of American Finance, an affiliate of the Smithsonian Institution, and sits on the editorial boards of Financial History magazine and The Journal of Behavioral Finance. A graduate of Columbia College, Jason lives in New York City.

Safal Niveshak (SN): What inspired you to write your latest book, The Devil’s Financial Dictionary? What’s the biggest lesson you wish the reader should take from the book?

Jason Zweig (JZ):

Ever since I was a college student, I’ve been an admirer of Ambrose Bierce, the 19th century American author who wrote The Devil’s Dictionary, one of the greatest works of satire in the English language.A few years ago, my teenage daughters were teasing me about how my personal website never featured anything new (at least in their opinion). I looked out the window of my home office and wondered: “What could I do that would be new every day without making readers feel that I’m encouraging them to respond to the market’s every move?”

To the left of my window, I glimpsed the paperback copy of The Devil’s Dictionary that I’ve owned since 1979. I glanced to the right and there, on my other bookshelf, was my second, hardcover copy of the same beloved book. I suddenly realized that I could write and post one satirical financial definition per day on my website. I didn’t expect it to turn into a book; I wrote the entries for fun. Then several publishers stumbled on it, and suddenly it became a book.

Of course, Wall Street and the rest of the financial world provide such a wealth of absurdities that eventually it may turn into a multi-volume encyclopaedia.

The lesson readers should take from the book is that the language of finance is often used not to explain, but to obfuscate. Those who know what terms mean can make a lot of money. Those who think they know what terms mean will lose a lot of money.

SN: What do you think happens inside our brains when we hear the financial experts’ gibberish? We all want to simplify our lives, so why is it that many of us admire those in the financial markets who throw at us the most complex stuff?

JZ: Neuroeconomist Gregory Berns of Emory University and his colleagues have found that listening to financial experts triggers a neural response they call “offloading,” which is a lower level of activation in the posterior cingulate and other regions of the frontal cortex normally engaged in decisions about risk and return. Conformity and deference to authority are part of human nature; man is a social animal, and we evolved to learn that following the leader and staying inside the herd helps to keep us alive. That served our ancestors well on the plains of the Serengeti. It doesn’t serve us well in modern financial markets, where computers can outsmart us and many people are richly rewarded for giving advice that is better for their own bottom line than it is for ours.

I also feel that financial jargon is even more insidious than other professional dialects, like medical lingo or info-tech gobbledygook. When a financial advisor uses jargon, we want to pretend to understand it so we can feel like privileged insiders who are “in the know.” Pretending to comprehend financial gibberish confers an illusion of power on those who purport to know what the jargon means.

In truth, the ultimate power lies in understanding that you don’t know what it means – and that the person using those words probably doesn’t, either.

SN: That’s true! Anyways, in mid-October 2016 front-page article in The Wall Street Journal titled The Dying Business of Picking Stocks, you wrote about investors giving up on stock picking and moving into passive funds. Can you please elaborate more in that? Do you see it as a long-lasting trend?

JZ: Our article was primarily about the U.S. market, although I believe these trends will inevitably percolate worldwide. Active management will never disappear entirely; hope springs eternal, and most people never entirely abandon their belief in magic.

Furthermore, active management gives investors someone else to blame. If you buy an index-tracking fund that loses 30% in six months, you have no one to blame but yourself; if you buy an actively managed fund that does the same, you can tell your family or your boss or your pensioners that the fund manager “strayed from his mandate.” You get to sack him instead of being sacked yourself. Finally, at least in the U.S. (and I’m sure in many other places), institutional investors are often required to make periodic “due-diligence” visits to the asset-management firms they hire. Many such firms seem to have home offices near beautiful beaches or in historic cities that are delightful to visit. Perhaps that is some kind of coincidence, but it certainly gives their largest clients a lifelong incentive to ignore high fees and low performance.

Nevertheless, index-tracking funds will continue to grow worldwide, as they should and as they must. Research by Fama and French, among others, has shown that nearly all outperformance relative to a market index can be explained by such common dimensions of risk and return as value, size, “quality” (profitability), and momentum. These factors can be systematically packaged into a tracker fund at extraordinarily low cost. An active manager whose success has come from picking stocks one at a time that score high on one or more of these factors must charge high fees to cover the considerable research costs; a passive fund can algorithmically mimic what the active manager is doing for a fraction of the cost. In the U.S., such “factor ETFs” are available for annual fees of under 0.1%, or 10 basis points and less. Active managers charging 10 to 20 times as much are doomed to lose market share.

SN: You define ‘forecasting’ as “an attempt to predict the unknowable by measuring the irrelevant; a task that in one way or another, employs most people on Wall Street.” Let’s talk about financial journalists here, who are in the prediction mode all the time, whether it’s newspapers, television, or the Internet. What role has financial journalism to play in promoting the devilish financial jargon you have defined in your book?

JZ: The financial media can’t be dissociated from the prediction industry in general. We are all guilty of perpetrating the myth that someone, somewhere, knows what the markets are about to do. Decades ago, the psychologist Paul Andreeassen showed that people who get more frequent news updates on their investment portfolios earn lower returns than those with no access to the news at all. That doesn’t mean that financial journalism is useless: Ignorance won’t make you a better investor. But the financial media should focus investors’ attention on the elements that separate success from failure – how to be optimally diversified, how to minimize fees and taxation, how to increase one’s own self-control – rather than pretending to clairvoyance or trumpeting whichever investment has been hottest lately.

I try to write for my high-school English teacher’s wife, who tells me whenever I see her that she likes my columns even though she doesn’t understand them. My goal is eventually to write one she can understand; I think, after 20 years, I am getting closer.

SN: You’ve defined “News” as “noise; the sound of chaos.” Bombarded with such noise from all sides, how does an investor go about blocking it to be able to make sound investment decisions.

JZ: Whatever can be a matter of policy and procedure must be. You should have a checklist that you must follow before taking any action. The rules should be yours, not mine, but they must be rules, not wishes. A few possibilities:

- Never buy a stock purely because its price has been going up, nor sell purely because it has been going down.

- List, in writing, three detailed reasons why you are buying, in terms that – like a scientific hypothesis – can be falsified by subsequent findings.

- Stipulate a price target, a time by which you expect the stock to reach that level, and an estimated probability that those forecasts are correct.

- Set up, in advance, automated alerts to remind you when price changes significantly – for example, 25%, 50%, etc. At those thresholds, assess methodically whether the value of the underlying business has changed comparably.

- Sign a contract with yourself, witnessed by family or friends, binding you to sell only when the value of the business, rather than the price of the stock, decays.

If that sounds like too much work, then owning individual stocks probably isn’t a good match for your temperament. Buy a passive fund instead – but don’t forget to sign a comparable contract with yourself.

SN: You recently quoted Keynes who said that courage is the key to investing. But showing courage when everyone is running for cover in a falling market is harder to do than to imagine. Given that such scenarios are playing out quite often in the current times, how does an investor build the necessary courage to combine with his/her capital when the opportunities come knocking?

JZ: Cash and courage go hand in hand, as Benjamin Graham wrote in 1932 after stocks had fallen more than 80%. Cash without courage will do you no good in a falling market, as you will be too afraid to invest it. Courage without cash is equally useless, as you can’t buy anything no matter how brave you feel if you have no money to buy it with. So husbanding some cash is the first step.

I am also great believer in what I call “financial fire drills.” Just as office-workers are periodically required to rehearse what to do if the building catches fire, investors should rehearse how they should behave if the stock market erupts in flames.

Build a watch-list of investments you would like to own at much lower prices than today’s, specifying the prices at which they will become bargains. Cultivate good mental hygiene now, before it is too late: Break bad habits like watching financial television, frequently checking the value of your brokerage accounts, or getting constant updates on the market. Go back and study your behavior during the last market crash: Did you sell? freeze? or buy more? (Don’t rely on your memory, which is likely to be illusory; consult your actual brokerage records, and be honest with yourself about what they show.) Then look at how those decisions worked out: Did your behavior rescue you from further losses, or preclude you from further gains?

Using what you learn about your past behavior, you should be able to structure rules to improve your future behavior.

SN: Your book basically mocks the outrageousness of the financial world which, in other words, is laying bare the truth of how the system works. In fact, you’ve defined “stock market” as a chaotic hive of millions of people who overpay for hope and underpay for value. Amidst all this, what advice do you have for a small, individual investor on how to safeguard his/her capital and grow his/her money?

JZ: The great investment philosopher Peter Bernstein liked to say that investors without much money should take small risks with most of their money and big risks with a little of it. Maximizing diversification should be your primary goal. If you put at least 90% of your investable assets into a small set of low-cost, widely diversified market-tracking funds, then there’s nothing wrong with trying to pick a few market-beating stocks with the rest of your money. You can’t lose much of your total wealth if you turn out to be incompetent at stock-picking, while you could enhance your wealth significantly if you turn out to be good at it. But you must be serious about it, willing to devote great amounts of time and effort and scholarship and emotional resolve. If you treat it as a game, you are certain to lose, sooner or later.

SN: How can an investor improve the quality of his/her decision making?

JZ: Study the markets. Study history. Study psychology. Above all, study yourself. Successful investing isn’t about picking the right stocks and avoiding the wrong ones. It is about making sure that you don’t let your own emotions deflect you from your strategy at the worst imaginable time. The best investors are those who think constantly about their own shortcomings and how to overcome them.

SN: What are the most important qualities an investor needs to survive the complexity of the financial markets?

JZ: Self-control. I don’t know what proportion of people who call themselves “investors” are, in fact, just speculators, but I wouldn’t be surprised if it is above 90%.

I find it remarkable that in India, the world’s wellspring of yoga, so many investors give themselves endless stress trying to chase short-term market performance.

Investing is not a 110-metre race. It is a marathon. If you want to finish the race, you shouldn’t try to go faster; you should slow down. And you need to learn how to resist investing in any asset or strategy you don’t understand.

SN: You talk about self-control. Can someone learn to have self-control or learn to behave well, if that attribute is not already ingrained in him/her? I’ve read this wonderful book called Sapiens, where the author talks about the gorging gene theory, which suggests that we carry the DNA from our ancestors of gorging on sugared or fatty food even when we have our refrigerators overstuffed with such foods. This is because our ancestors used to gorge on sugared fruits but that was purely out of scarcity and fear that if they did not eat them, the baboons would. So, with such a DNA, can we as investors really learn to behave well?

JZ: Genetics is predisposition, but it doesn’t have to be predestination. We’re all inclined to love sweet, salty, or fatty foods, but we aren’t all doomed to like them. With diligence and discipline, we can train ourselves to have higher resistance to them. And we can recognize that willpower is insufficient, in and of itself, to achieve that resistance. We must make our environment more hygienic. Think of alcoholics, for example. You might tell yourself, When someone offers me a drink, I will just say no. But, over time, you will learn that that doesn’t work, because of what psychologist George Lowenstein has called “the hot-cold empathy gap”: In a cold, or emotionally unengaged state, you will picture your future desires as much more manageable than they will, in fact, turn out to be in the heat of the moment. So eventually alcoholics learn to control their environmental hygiene: They avoid walking down the street where the tavern is, they ask their friends to tell the party host not to serve alcohol, they bring their own non-alcoholic beverages with them when they travel. All of those behaviors are intended to keep dangerous emotional cues at bay.

By the same token, investors need to avoid the cues that can trigger self-defeating behaviors. Use checklists and watchlists to prevent impulse from determining your behavior. Remove any trading apps from your smartphone. Don’t bookmark any websites that encourage you to update your account values in real time. Build a spreadsheet of all your holdings that you refresh only once every calendar quarter. Change the password on your brokerage account to a personalized variant of IWILLTRADEONLYWHENABSOLUTELYNECESSARY; there is evidence from psychological research that frequent subliminal repetition of such a message can change your behavior.

You should be under no delusion that these techniques will eliminate your genetic frailties. But they can help you exert at least some control over them.

SN: Are successful investors born, or made?

JZ: Both, of course. A great deal of investing success comes from temperament, which is (largely) inborn. But every good investor I’ve ever met is a learning machine – someone who eats information ravenously and who is obsessed not by how much he already knows but by how much he has yet to learn.

An underappreciated factor that great investors share, I believe, is that they relish being proven wrong. Most people dread making mistakes with a kind of visceral horror. But great investors welcome making mistakes, because errors are opportunities to learn. Whenever I encounter a professional investor with a track record of outperformance who boasts only about what he got right, I know I am in the presence of someone whose overconfidence is dangerous, if not deadly.

SN: Apart from Ben Graham, Warren Buffett, and Charlie Munger, who inspires you the most when it comes to investing and investment behaviour?

JZ: I would name three people: two giants and one few people have ever heard of. First, John Maynard Keynes: Chapter 12 of his book The General Theory of Employment, Interest and Money is probably the most concentrated set of profound insights into investment behavior ever written. He teaches us that to be rational you must reckon with how irrational other people can be.

Second, Daniel Kahneman, whom I have known for 20 years and whose book Thinking, Fast and Slow I helped research, write and edit: From Danny I learned how important it is to try answering difficult questions by beginning with the words “I don’t know.” The admission of ignorance is the gateway to learning, and the more you learn the clearer it should become to you how much you do not know. Finally, an individual investor and retired U.S. Army colonel named Jack Hurst, whom I met when amyotrophic lateral sclerosis (motor neurone disease) had already paralyzed his entire body save a few muscles in his right cheek. Unable to speak or move on his own, Jack nevertheless exemplified the patience, skepticism, independence, discipline, and courage that characterize the intelligent investor. Using a computer-brain interface powered by the electrochemical signals in the facial muscles over which he still had voluntary control, he meticulously researched stocks, bought them after severe price declines, sold them to capture tax benefits, and watched financial television – but with the sound turned off so it wouldn’t influence him emotionally! I wrote about him here. He taught me that courage is the most underappreciated of all investing virtues.

SN: You have inspired millions through your writing, but which are some of the books on investing, behaviour, and multidisciplinary thinking that have inspired you the most over the years? If you were to give away all your books but one, which one would it be and why?

JZ: I have listed the books I regard as indispensable here, here, and here.

Your last question is painfully difficult for someone who has loved books since he first learned to walk. I suppose if you held a gun to my head and made me pick only one book to keep, it would be the Essays of Montaigne. While that book has nothing to do directly with investing, it has everything to do with learning how to think and live. I can’t think of another book that is so good a guide to what it means to know oneself, to embrace uncertainty, to live within one’s means, to value humility above all other virtues, and to remember that the two greatest intellectual endeavours in life are to learn as much as possible and to accept how little you will ever be able to learn.

SN: Hypothetical Question: If you had a magic wand, which ill of the financial system would you eliminate first, and why?

JZ: I suppose I would require anyone providing investment advice to have a formal fiduciary duty to the client. Enforcing that requirement would be difficult, however. The supply of people whose minds and hearts qualify them to be fiduciaries for others is probably insufficient to meet even one-tenth of the demand. The sudden imposition of such a requirement would force millions of advisors around the world to try meeting a standard that most would fall short of. Perhaps there should be some sort of centralized training and licensing regime, the same way most nations require physicians, attorneys, and accountants to meet rigorous professional standards. Unfortunately, the magic wand you have handed me doesn’t seem to work; we are probably many years, if not decades, away from seeing fiduciary duty become universal. That is a shame. Investors, in the meantime, will have to rely largely on themselves; identifying good financial advisors is going to require great effort for the foreseeable future.

SN: You’ve talked about the importance of being a learning machine. And it seems that reading widely – apart from learning from, say, role models – is one of the important means to becoming a learning machine. In this regard, what are your thoughts on how one should go about selecting which books to read? There are so many books that come out these days, and each one of them looks inspiring and highly recommended by someone. But time is limited. So, is restricting to the supertexts on investing, thinking, and behaviour a good idea? Else, how should one go about selecting which new books to read? Do you have such a process in place?

JZ: I don’t have a formal process. However, I do pay close attention to what the people I respect the most are reading. When someone I admire recommends a book or a website or anything else to read, I try to read it. If minds better than mine have benefited from something, then so can I. It’s also worth bearing in mind that people without high standards will often recommend reading something that sounds better than it is. It’s disconcertingly easy for anyone to write a review or summary of just about anything and make it sound exciting even if, in fact, it is barely better than garbage. So if (for example) Charlie Munger says a book is “not bad,” you should regard that as much higher praise than if a second-rate or third-rate mind says some other book is a “must-read” or a “masterpiece.”

SN: As I’ve read at a few places, you also seem to hold Richard Feynman in very high regard. What are some of the most important things you like about Mr. Feynman and his teachings, which readers of this interview could also benefit from?

JZ: What I love about Feynman was his determination to think for himself and to be honest about his own limitations. In his books, he tells remarkable stories that can help even humanists think like scientists.

When Feynman was young, his wife, Arlene, was dying. Every day, she would send him little gifts at his office to show how much she loved him. Among them were bespoke pencils she’d had made with lettering along the lines of “I LOVE YOU, RICHARD. ARLENE.” (I don’t remember the exact wording, but it was something like that.) Embarrassed lest his colleagues see these emotional messages on his pencils, Feynman scraped them off with a knife. Soon, the next round of pencils arrived. This time, the message on them read: WHAT DO YOU CARE WHAT OTHER PEOPLE THINK?” From that, he – and all his readers since then – have learned the importance of disregarding the opinions of others when important matters of the heart (or mind) are at stake. My other Feynman story involves the time he was asked by the state of California to sit on the committee that approves science textbooks for schoolchildren. He requested a copy of every single book on the list and read each from cover to cover. At the final committee meeting, the other members all said their favorite book was X. To Feynman’s astonishment, they had picked the book with the prettiest cover but without a word of text. It turned out that none of them had even opened the textbook; they liked how the cover looked and picked it as “best” on that basis alone. From that I learned the importance of always reading the source material, rather than relying on someone else’s representation of it. It still amazes me how many people who say “studies have shown that…” have never read the studies they are citing.

SN: Can you name some of the current publications (newspapers, magazines, blogs etc.) you read and respect a lot for their learning quotient? As far as reading newspapers is concerned, there have been proponents (like Warren Buffett who say it is a great source of ideas and information) and opponents (like Taleb who think newspapers are plain noise) of the same. Which side are you on? Is there a way to read newspapers effectively to differentiate between noise and signal?

JZ: I’ve listed many of the sources I regularly read here. Nowadays, I don’t use the term “newspapers” much; I call them (including The Wall Street Journal) “news organizations,” because that’s what we are. We don’t only, or even primarily, publish a newspaper. We publish online and on your phone and by email and so forth. To be honest, I don’t believe there is much debate to be had on this matter. Just ask yourself: Would I be able to make better decisions if I knew nothing whatsoever about what is happening in the world around me? It seems to me that the question answers itself, in the negative. While most investors probably pay too much attention to the news, an investor who pays no attention at all would be entirely in the dark.

As for me, I read The Wall Street Journal in both print and electronic form. First thing in the morning and last thing at night, I whiz through the top stories of the day on my iPhone to get a quick feel for what is happening. When I arrive at my desk for the work day, I read the print edition. I find that the “What’s News” column on Page One, which provides a one-or-two-sentence summary of every important article, is an invaluable guide to focusing my attention. Then I will often open some of the stories in my Internet browser, since the online versions often have interactive features that the print versions don’t. However, I don’t read every article every day; far from it. I focus on a handful that interest me, some in finance, some in politics or economics, some in technology, some in culture. On the weekend I mainly read our coverage of history and culture. The only other observation I would make is that when I am not working, I am always reading – but never about work. In my spare time away from the office, I have an iron rule never to read anything relating to finance or economics. Instead, I read classic fiction, poetry, history, philosophy, or science. The mind, like any muscle, must rest in order to grow. If all you read is finance, morning, noon, and night, eventually you will stop being able to learn anything new about finance. The best way to deepen your mastery of specific knowledge is by broadening your horizons of general knowledge.

SN: On that wonderful note, Jason, let me thank you for sharing your amazing and deep insights for Safal Niveshak readers. I’m sure readers are going to attain great benefits out of your thoughts and experience.

JZ: Thanks for the interview, Vishal! I really enjoyed it.

Note: This interview was originally published in the December 2016 issue of Value Investing Almanack. To read more such interviews and other deep thoughts on value investing, business analysis and behavioral finance, click here to subscribe to VIA.